by Savi3

by Savi3Space is no longer exploratory. It is becoming foundational.

Capital that enters early shapes the ecosystem.

Space is transitioning from exploration to critical global infrastructure, driven by mega constellations, AI compute demand, and geopolitical resilience.

1. Executive Summary

- The space economy is entering a scale phase, comparable to early telecom fiber and cloud data centers.

- Governments, hyperscalers, and private capital are simultaneously deploying tens of thousands of satellites.

- New frontier: space-based data centers, AI compute, and ultra-resilient global networks.

- Multi-trillion-dollar opportunity over the next 10–20 years across infrastructure, services, and platforms.

2. Why Now?

Key irreversible forces:

- Exploding Data & AI Demand

- AI data centers are constrained by power, cooling, land, and regulation on Earth.

- Orbital compute offers solar energy, passive cooling, and global distribution.

- Geopolitical & Sovereignty Needs

- Governments need secure, independent satellite networks (EU IRIS², China SatNet).

- Space infrastructure is now viewed as strategic national infrastructure.

- Cost Curve Inflection

- Reusable launch (SpaceX, Blue Origin) reduced launch costs by >80% vs 2010s.

- Satellite manufacturing moving toward mass production.

3. Market Size & Growth

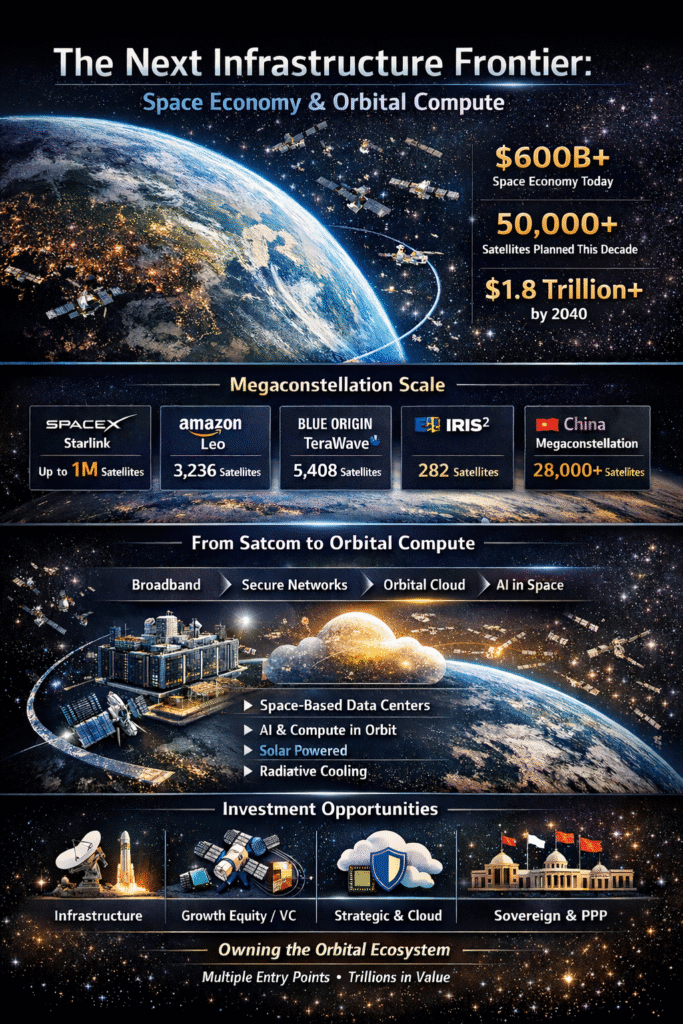

- Global space economy: $300B in 2014. ~$660B today; projected to exceed $1.8T+ by mid 2030 (industry consensus).

- Satellite broadband & data networks: projected $50B+ annually by early 2030s.

- AI data center market: projected $400B+ by 2030, with orbital compute emerging as an extension.

- Venture & private investment in space: $8–10B annually, accelerating.

4. Mega constellation Landscape

Commercial

- SpaceX Starlink: 9,000+ satellites live; licensed for 12,000+, with filings up to 34,400.

- SpaceX Orbital Data Center Filing: FCC application for up to 1,000,000 satellites (AI & compute).

- Amazon Leo (Kuiper): 3,236 satellites approved.

- Blue Origin TeraWave: ~5,408 satellites (enterprise & high-throughput networking).

- Starcloud: FCC filing for ~88,000 satellites for orbital data centers.

Government / State-Backed

- EU IRIS²: ~282 satellites; €10.5B budget.

- China Guowang + Qianfan: ~28,000+ satellites planned.

- China explicitly includes space-based data centers in state planning.

5. Shift From “Satcom” to “Space Infrastructure”

Past:

- Voice, TV, niche broadband

Present:

- Global broadband, IoT, defense, mobility

Next:

- AI compute in orbit

- Distributed cloud & edge processing

- Space-based data centers

- Ultra-secure, sovereign networks

| Space is becoming the fourth compute domain (after cloud, edge, on-device).

6. Investment Opportunity Map

Layered Value Stack

- Launch & Access

- Reusable rockets, rideshare, orbital transfer vehicles

- Satellites & Manufacturing

- Mass-manufactured spacecraft

- Radiation-hardened chips, propulsion, thermal systems

- Networks & Platforms

- Satcom, optical inter-satellite links

- Orbital cloud platforms

- Compute & Data

- Space data centers

- AI inference & training in orbit

- Ground & Integration

- User terminals, gateways, edge data centers

- Cloud & telco integration

- Governance & Safety

- Space traffic management

- Cybersecurity, debris mitigation

7. Where To Participate

- Growth Equity / Late VC

- Satellite operators

- Orbital compute startups

- Space networking platforms

- Infrastructure Capital

- Ground stations & gateways

- Launch & manufacturing capacity

- Space-enabled data infrastructure

- Strategic & Corporate VC

- Cloud providers integrating orbital compute

- Defense & secure communications

- Energy + space hybrid systems

- Public Markets & Thematic Exposure

- Listed satellite operators

- Aerospace & space manufacturing leaders

- Space-focused ETFs & indices

- Consortium & PPP Models

- Government-backed programs (IRIS²-like models)

- Sovereign space infrastructure funds

8. Strategic Call to Action

The winners will not be those who pick one constellation, but those who own positions across the space infrastructure ecosystem.